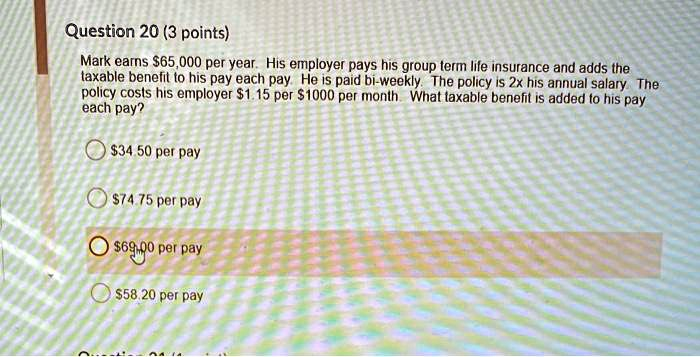

The Correct Answer and Explanation is:

ased on the information provided in the image, the correct answer is $69.00 per pay.

Explanation

This problem requires a step-by-step calculation to determine the portion of the employer-paid life insurance cost that is added as a taxable benefit to each of Mark’s paychecks. Here is a detailed breakdown of the calculation process.

1. Calculate the Total Life Insurance Coverage

First, we need to determine the total value of the life insurance policy. The problem states that the policy is for an amount equal to two times Mark’s annual salary.

- Mark’s annual salary: $65,000

- Policy coverage multiplier: 2

- Total coverage amount: 2 * $65,000 = $130,000

So, Mark has a group term life insurance policy with a death benefit of $130,000.

2. Calculate the Monthly Cost of the Policy

Next, we calculate the cost that the employer pays for this policy each month. The cost is given as $1.15 per $1000 of coverage per month. To find the total monthly cost, we must first determine how many thousands of dollars are in the total coverage.

- Number of $1000 units in the policy: $130,000 / $1,000 = 130 units

- Cost per unit: $1.15

- Total monthly cost: 130 units * $1.15/unit = $149.50

The employer pays $149.50 each month for Mark’s life insurance policy.

3. Calculate the Total Annual Cost

To determine the amount per paycheck, it is helpful to first find the total cost of the benefit over a full year. We can do this by multiplying the monthly cost by the number of months in a year.

- Total annual cost: $149.50/month * 12 months = $1,794

This $1,794 is the total taxable benefit Mark receives from this insurance policy over the course of one year.

4. Determine the Taxable Benefit Per Pay Period

Finally, we need to distribute this annual cost evenly across Mark’s pay periods. The problem states he is paid bi-weekly. There are 52 weeks in a year, which means there are 26 bi-weekly pay periods in a year (52 weeks / 2 weeks per period = 26 pay periods).

- Annual taxable benefit: $1,794

- Number of pay periods per year: 26

- Taxable benefit per pay period: $1,794 / 26 = $69.00

Therefore, $69.00 is the taxable benefit that is added to Mark’s gross pay for each bi-weekly pay period. This value matches the third option provided in the question.