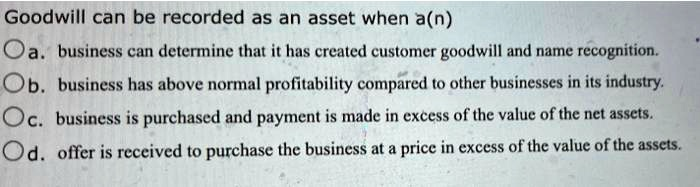

Goodwill can be recorded as an asset when a(n) a. business can determine that it has created customer goodwill and name recognition. b. business has above normal profitability compared to other businesses in its industry. c. business is purchased and payment is made in excess of the value of the net assets. d. offer is received to purchase the business at a price in excess of the value of the assets.

The Correct Answer and Explanation is:

The correct answer is C. business is purchased and payment is made in excess of the value of the net assets.

Explanation:

In accounting, goodwill is a unique intangible asset that represents the value of a company’s non-physical attributes, such as brand reputation, a strong customer base, good employee relations, and proprietary technology. While these factors are undeniably valuable, accounting principles require objective and verifiable evidence before an asset can be recorded on the balance sheet.

The only circumstance under which goodwill can be officially recorded as an asset is during a business acquisition. When one company purchases another, the acquiring company pays a certain price. This purchase price is first allocated to all the identifiable tangible and intangible assets (like equipment, inventory, patents) and liabilities of the acquired company, all measured at their fair market value. The “net assets” are the fair value of these identifiable assets minus the fair value of the liabilities.

If the purchase price paid is higher than the fair value of these net identifiable assets, the excess amount is recorded as goodwill. This is known as purchased goodwill. For example, if Company A buys Company B for $10 million, and the fair value of Company B’s net identifiable assets is $8 million, then Company A would record $2 million as goodwill on its balance sheet. This $2 million represents the premium paid for those unidentifiable qualities that make Company B attractive, such as its market position or customer loyalty.

Option A is incorrect because internally generated goodwill, such as creating name recognition over time, cannot be recorded. Its value is too subjective and difficult to measure reliably without a market transaction.

Option B is incorrect because while above-normal profitability may be an indicator that a company possesses goodwill, it is not the event that triggers its recording.

Option D is incorrect because receiving an offer is not a completed transaction. Accounting records are based on actual events, not potential or future ones. An offer can be rejected or withdrawn, so it does not provide a basis for recording an asset.