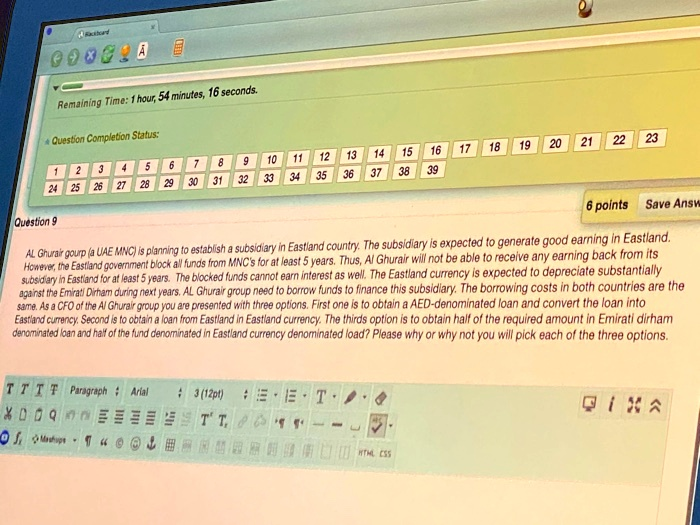

Remaining Time: 1 hour, 54 minutes, 16 seconds. Question Completion Status: 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 6 points Save Answ Question 9 AL Ghurair gourp (a UAE MNC) is planning to establish a subsidiary in Eastland country. The subsidiary is expected to generate good earning in Eastland. However, the Eastland government block all funds from MNC’s for at least 5 years. Thus, Al Ghurair will not be able to receive any earning back from its subsidiary in Eastland for at least 5 years. The blocked funds cannot earn interest as well. The Eastland currency is expected to depreciate substantially against the Emirati Dirham during next years. AL Ghurair group need to borrow funds to finance this subsidiary. The borrowing costs in both countries are the same. As a CFO of the Al Ghurair group you are presented with three options. First one is to obtain a AED-denominated loan and convert the loan into Eastland currency. Second is to obtain a loan from Eastland in Eastland currency. The thirds option is to obtain half of the required amount in Emirati dirham denominated loan and half of the fund denominated in Eastland currency denominated load? Please why or why not you will pick each of the three options.

The Correct Answer and Explanation is:

Here is the strategic evaluation of each financing option for Al Ghurair group:

Option 1: Obtain an AED-denominated loan and convert to Eastland currency

This option exposes the firm to significant exchange rate risk. Since the Eastland currency is expected to depreciate substantially against the AED, the funds converted now may lose value over time, reducing the real value of earnings when repatriation eventually becomes possible. Additionally, repayments would be in AED, but the subsidiary’s income will be in the weakening Eastland currency, heightening the risk of a currency mismatch.

Option 2: Obtain a loan from Eastland in Eastland currency

This approach aligns the loan currency with the operational currency. Since the earnings and repayments are both in Eastland currency, it eliminates exchange rate risk. It is financially sound given that returns are blocked and cannot be transferred or earn interest. However, the value of the locked-in earnings will deteriorate in real terms due to currency depreciation. This option limits exposure to external currency volatility but accepts inflation and devaluation losses.

Option 3: Split financing between AED and Eastland currency

This option balances currency risk and operational alignment. Borrowing half in AED spreads risk across two currencies while still allowing partial alignment of liabilities with the operating currency. It reduces total exposure to either extreme. Though it does not eliminate currency risk, it hedges part of it by diversification. Given uncertainty in future currency trends and the inability to repatriate funds, this is a more flexible and prudent approach.

Recommendation: Option 3 is the most balanced and risk-aware strategy under the current circumstances. It allows some protection against devaluation while limiting exposure to potential currency mismatch in repayment. Diversifying financing sources provides adaptability in a volatile economic setting.